Guide to Best Health Insurance in Singapore

One of the quintessential Singaporean healthcare must-haves is having MediShield Life – a basic health insurance which covers basic public hospital treatments, and you can choose to supplement your MediShield Life with an Integrated Shield Plan (IP) as well. In this guide, we’ll look at what types of health insurance plans are available, who is it suitable for and how to get it.

How Does Health Insurance Work in Singapore?

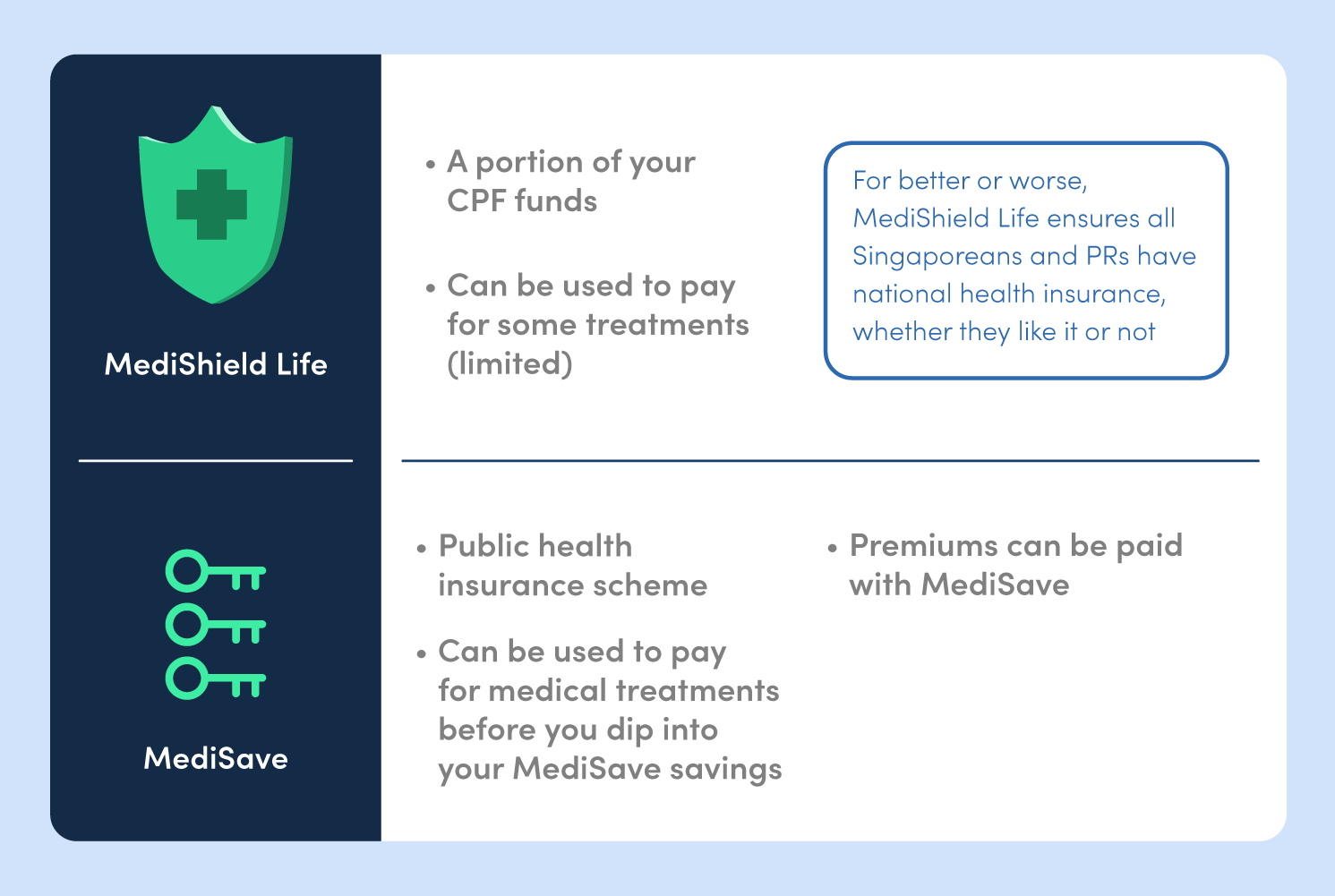

Medishield vs Medisave: What's The Difference?

Health Insurance vs. Life Insurance

Health Insurance

- Covers the costs of healthcare in Singapore, including hospital bills, medical treatments and other health-related expenses.

- All Singaporeans and PRs already have basic health insurance coverage which is MediShield Life and the premiums are paid through your CPF MediSave account.

- There are 4 types of health insurance plans namely, MediShield Life, Integrated Shield plan (IP), international health insurance (local provider), international health insurance (global provider).

- MediShield Life is the most basic type of health insurance, so it covers only the lower wards like Class B2 and C, surgery coverage is capped at $2,600, does not cover post-hospitalisation treatments, but MediShield Life can be supplemented with an IP.

- IPs covers you at A wards or even private hospitals but it comes at a higher premium which can be deducted from your CPF MediShield (up to the MediShield withdrawal limits).

- IP riders are available as well so you can “add on” these riders to your place to get wider coverage and you’ll need to pay for these extras with cash.

- International health insurance plans by local and global providers provide wider coverage such as regional or worldwide coverage.

- Inpatient and outpatient treatments, routine check-ups, chronic conditions, maternity coverage, newborn coverage, dental benefits, vision coverage, evacuation and repatriation coverage, are usually included in international health insurance plans.

Life Insurance

- Gives you a payout known as “sum assured” when you get into an accident, suffer an injury, total permanent disability (TPD) or death. The payout varies according to how severe the outcome is.

- Purpose of having this type of insurance is to compensate for your reduced earning ability.

- More suitable if you’re planning to have children, or if you have other dependents such as siblings or parents, so as to help your dependents get by while you’re unable to work.

- There are two types of life insurance, namely whole life insurance and term insurance.

- Term life insurance has lesser coverage than whole life and the premiums are much lower. It usually insures you for the duration you prefer (10 to 30 years). However, you will not be able to receive any payout if you survive the term (no accidents or death).

- Whole life insurance covers you for life and is a lot more pricey, but there is a cash payout you can get at some point during the whole life insurance coverage period.

What Is The Best Health Insurance Plan in Singapore?

| PLAN | INSURER | FOR |

|---|---|---|

| HealthShield Gold Max | AIA | Inpatient/Day surgery, outpatient treatment |

| PRUShield | Prudential | Pre and post hospitalisation, Inpatient/Day surgery |

| IncomeShield | Income | Outpatient treatment, organ transplant |

| SupremeHealth | Great Eastern | Outpatient treatment, high claim limit per policy year |

| Shield | AXA | Cheapest premium, emergency overseas treatment |

| Raffles Shield | Raffles Health Insurance | High claim limit per policy year, pre and post hospitalisation |

Why is health insurance necessary?

What is health insurance and why do you need it? Health insurance serves to protect you from one of the biggest financial risks you might ever face – healthcare expenses. Essentially, health insurance means protection from hospitalisation and medical costs, as well as medical bills arising from injuries, illnesses, or disabilities. TL;DR? All it takes is one expensive accident or illness to wipe out your savings and retirement funds. Therefore, you will need health insurance to deal with the ever-increasing healthcare costs.

Healthcare Inflation

![]() One phrase you need to know is healthcare inflation. Inflation basically drives up prices of goods and services by around 3% each year. Healthcare inflation, on the other hand, runs up to 2 or 3 times that general inflation rate. Why? That’s because advances in medicine, medical research, and medical technology are costly. In fact, these are the 3 main factors driving healthcare costs in Singapore today.

One phrase you need to know is healthcare inflation. Inflation basically drives up prices of goods and services by around 3% each year. Healthcare inflation, on the other hand, runs up to 2 or 3 times that general inflation rate. Why? That’s because advances in medicine, medical research, and medical technology are costly. In fact, these are the 3 main factors driving healthcare costs in Singapore today.

Short Hospitalisation

![]() If you fall ill, get hospitalised for 3 weeks on no-pay leave, and receive a S$40,000 medical bill upon check-out, your health insurance plan should be able to absorb a huge chunk of those healthcare costs for you. You may end up paying 5%, and another S$1,500 or so in deductibles (you will learn about this later) – but the rest will be "paid" by your insurance company. This way, you don't have to empty your bank account and borrow from your family, friends, and loan sharks to pay your hospital and medical expenses.

If you fall ill, get hospitalised for 3 weeks on no-pay leave, and receive a S$40,000 medical bill upon check-out, your health insurance plan should be able to absorb a huge chunk of those healthcare costs for you. You may end up paying 5%, and another S$1,500 or so in deductibles (you will learn about this later) – but the rest will be "paid" by your insurance company. This way, you don't have to empty your bank account and borrow from your family, friends, and loan sharks to pay your hospital and medical expenses.

Long-Term Illness

![]() If you are a sole breadwinner who got diagnosed with a terminal or critical illness (touch wood!), are forced to stop working, and unfortunately pass on, you'll be leaving your spouse, parents, or children behind with no source of income – and hefty medical expenses to foot. Your life insurance plans will give them lump-sum payout cheques to help them continue with their lives for a short period (while they find new sources of income) – basically protecting their financial stability for a year or two.

If you are a sole breadwinner who got diagnosed with a terminal or critical illness (touch wood!), are forced to stop working, and unfortunately pass on, you'll be leaving your spouse, parents, or children behind with no source of income – and hefty medical expenses to foot. Your life insurance plans will give them lump-sum payout cheques to help them continue with their lives for a short period (while they find new sources of income) – basically protecting their financial stability for a year or two.

Looking for something more specific?

Should You Buy Additional Health Insurance Coverage?

A common reason why some Singaporeans do not purchase additional healthcare coverage is because they already have enough coverage with MediShield and their employer’s insurance scheme. Yet, everyone’s health needs and insurance may different – you should check your insurance policies for gaps, limitations and exclusions. So, before you assume that your current health insurance policies are sufficient, evaluate your total coverage, look for gaps, and consider purchasing additional health insurance coverage to cover those bases and reduce your risk of running into an unpaid hefty medical bill.

Should You Get Private Health Insurance?

If you’re have family history of health problems or you’re an expat staying or working in Singapore (with or without your family members here), it’ll be better to get a more comprehensive health insurance plan instead of just relying on your employee insurance, as Singapore’s high healthcare costs may be challenging to afford if your income is not high enough to cover.

Family history of health issues

It is always safer to get coverage against any health risks, especially if you know that your family members have health issues which may or may not be hereditary. By getting private health insurance plans to supplement your MediShield Life (if you’re Singaporean or PR), you can avoid excessive health expenses. This is the same for expats staying in Singapore. Unforeseen circumstances of you falling ill or getting into an accident can happen, so it is still safer to be insured against any possibilities.

Limited coverage provided by the employer

Although many companies provide a group health insurance plan to cover their employees, there is no guarantee that the coverage is extensive enough for each employee and their family members, whether you’re Singaporean, PR or a foreigner in Singapore. So, by having a private health insurance plan that is tailored to the specific needs of your health condition, it will help reduce the overall healthcare costs for you and your family whenever necessary.

Frequent travel required

As a Singaporean, PR or a foreigner in Singapore, if you need to travel to various countries (or a particular country outside of Singapore) often for your work or other commitments, getting an international health insurance plan will be useful as you will receive medical coverage 24/7 wherever you fly to. International health insurance coverage is usually enough but sometimes having a travel insurance plan to complement your health insurance plan may be needed to suit your requirements as someone who travels a lot.

Which Insurance Plan Is Right For You? Hear From Our MDRT-Qualified Specialists.

From health insurance to life and term insurance, getting your insurance portfolio in order is probably one of the best things you can do for your finances, especially while you're still young.

To help you make sense of this, MoneySmart Financial's MDRT-certified team of experts is here to give you a hand, with insightful tips on choosing between the different insurance plans, access to comprehensive research, price comparisons, eligibility, or documentation, and ultimately enjoying a seamless insurance selection and application journey.

Did you know the Million Dollar Round Table founded in 1927 serves as an international association uniting various financial professionals, including life insurance agents, financial advisors, and wealth managers? The MDRT recognition is regarded as a mark of distinction, with specific benchmarks for excellence.

What Customers Say about their Health Insurance Purchase

Review by Filippo Lombardi

Review by Abby Ling

Get your personalised Insurance Plan here

What types of Health Insurance are there?

Types of Health Insurance in Singapore

Hospital Income Insurance

![]() Hospital income insurance offers you a fixed amount of cash daily (e.g. S$250) from the insurer for each day you’re hospitalised, up to a maximum number of days (e.g. 365 days) per accident or illness.

Hospital income insurance offers you a fixed amount of cash daily (e.g. S$250) from the insurer for each day you’re hospitalised, up to a maximum number of days (e.g. 365 days) per accident or illness.

Long-Term Care Insurance

![]() Long-term care insurance offers you a fixed amount of cash monthly (e.g. S$400) for long-term nursing care that typically includes assistance with daily activities such as bathing, dressing, and feeding. This coverage is often offered by insurers in the form of ElderShield supplements.

Long-term care insurance offers you a fixed amount of cash monthly (e.g. S$400) for long-term nursing care that typically includes assistance with daily activities such as bathing, dressing, and feeding. This coverage is often offered by insurers in the form of ElderShield supplements.

Disability Income Insurance

![]() Disability income insurance offers you “income replacement” of up to a certain percentage of your gross monthly income. So, if you’re making S$5,000 a month, your insurer might allow you to insure 80% (varies by insurer) of your income – meaning in the event of an accident that leaves you disabled, your monthly payout would be S$4,000 until you’re able to perform your duties once again.

Disability income insurance offers you “income replacement” of up to a certain percentage of your gross monthly income. So, if you’re making S$5,000 a month, your insurer might allow you to insure 80% (varies by insurer) of your income – meaning in the event of an accident that leaves you disabled, your monthly payout would be S$4,000 until you’re able to perform your duties once again.

Hospitalisation Insurance

![]() Hospitalisation insurance offers you reimbursement from the insurer for any medical expenses, treatment bills, and hospitalisation costs. Depending on the policy, the coverage you receive may either be full or limited.

Hospitalisation insurance offers you reimbursement from the insurer for any medical expenses, treatment bills, and hospitalisation costs. Depending on the policy, the coverage you receive may either be full or limited.

Critical Illness Insurance

![]() Critical illness insurance offers you a lump sum payment from the insurer to help alleviate hefty medical expenses in the event you are diagnosed with a critical illness such as cancer, heart attack, kidney failure, coma, etc. The list of qualifying critical illnesses varies by insurer.

Critical illness insurance offers you a lump sum payment from the insurer to help alleviate hefty medical expenses in the event you are diagnosed with a critical illness such as cancer, heart attack, kidney failure, coma, etc. The list of qualifying critical illnesses varies by insurer.

Terminal Illness Insurance

![]() Similar to critical illness insurance plans, a terminal illness insurance plan gives you a lump-sum payout if your doctor diagnoses you with a terminal illness – meaning you are down with an end-stage illness and have been given a limited amount of time to live.

Similar to critical illness insurance plans, a terminal illness insurance plan gives you a lump-sum payout if your doctor diagnoses you with a terminal illness – meaning you are down with an end-stage illness and have been given a limited amount of time to live.

Compare Health Insurance Plans now

What to Consider Before Choosing an Integrated Shield Plan?

Cost of premiums

When you are considering to purchase an insurance health plan, first budget your finances to ensure you can sustainably afford the monthly premiums for the next couple of years. Note that monthly premiums will be for the IP (Medisave-payable) and the co-payment rider. Next, ensure you will be able to afford future premiums which will be higher than your current premiums. Health insurance premiums increase constantly for 2 reasons: as you age, your health risks increase; healthcare and medical costs are always advancing and on the rise.

Coverage

While cost of an insurance plan is something you definitely have to consider, you should not just settle for the cheapest plan you see. This way, you may be compromising on the healthcare coverage you receive. Instead, you should consider looking for a plan that fits your budget and provides extensive coverage. However, an insurance plan with high and all-encompassing healthcare coverage may come with hefty premiums and require you to pay more than what you can sustain in the long term. You will want to strike a practical balance here.

Pre and Post Hospitalisation coverage

Some IPs differ in length of coverage so it is better to ensure your IP covers a longer period of hospitalisation for your benefit.

Why get an Integrated Shield Plan?

You may have MediShield and your company’s insurance plan under your belt but that doesn't guarantee comprehensive healthcare coverage for you. The only way to ensure you’ll have 100% adequate coverage is to identify any gaps in your existing policies and seek out relevant health insurance policies to bridge those gaps.

Higher claim limits

![]() An Integrated Shield Plan (IP plan) basically serves to increase your annual claim limit for your MediShield Life plan – therefore increasing your healthcare coverage. MediShield Life's annual claim limit is only S$100,000 but an Integrated Shield Plan's annual claim limit may run up to S$1,000,000 instead. With the increase in claim limit, you will also be covered for a wider range of healthcare conditions, more ward classes, pre- and post-hospitalisation expenses, and medical coverage outside of Singapore.

An Integrated Shield Plan (IP plan) basically serves to increase your annual claim limit for your MediShield Life plan – therefore increasing your healthcare coverage. MediShield Life's annual claim limit is only S$100,000 but an Integrated Shield Plan's annual claim limit may run up to S$1,000,000 instead. With the increase in claim limit, you will also be covered for a wider range of healthcare conditions, more ward classes, pre- and post-hospitalisation expenses, and medical coverage outside of Singapore.

Higher ward classes

![]() The basic MediShield Life provides Singaporeans and Permanent Residents (PRs) with coverage for Class B2 and C wards in public hospitals. While you can still opt to stay in Class A or B1 wards, it requires you to top-up the excess cost. This is one of the reasons why individuals may opt for an Integrated Shield Plan (IP) – so that they can have insurance coverage for higher-tier wards in public and private hospitals. A higher-tier ward or access to private hospitals may reduce your waiting time for access to medical treatments and hospitalisation.

The basic MediShield Life provides Singaporeans and Permanent Residents (PRs) with coverage for Class B2 and C wards in public hospitals. While you can still opt to stay in Class A or B1 wards, it requires you to top-up the excess cost. This is one of the reasons why individuals may opt for an Integrated Shield Plan (IP) – so that they can have insurance coverage for higher-tier wards in public and private hospitals. A higher-tier ward or access to private hospitals may reduce your waiting time for access to medical treatments and hospitalisation.

Agent

![]() Another plus point that people like about getting an Integrated Shield Plan is the access to an insurance agent. Your agent is your point of contact for anything health insurance-related. Hence, when you need to make a claim or check your coverage, you can simply drop your agent a text or call instead of browsing through multiple hospital and government websites.

Another plus point that people like about getting an Integrated Shield Plan is the access to an insurance agent. Your agent is your point of contact for anything health insurance-related. Hence, when you need to make a claim or check your coverage, you can simply drop your agent a text or call instead of browsing through multiple hospital and government websites.

MediShield Life

![]() MediShield Life, for instance, is a mandatory health insurance offered by Singapore's Ministry of Health (MOH), with coverage for all Singaporeans and Permanent Residents (PRs) – but it has its limitations such as a S$100,000 claim limit per year, access to only class B2 and C wards in public hospitals, no coverage for maternity-related conditions, hospice, and moreAn Integrated Shield Plan (IP plan) basically serves to increase your annual claim limit for your MediShield Life plan – therefore increasing your healthcare coverage. MediShield Life's annual claim limit is only S$100,000 but an Integrated Shield Plan's annual claim limit may run up to S$1,000,000 instead. With the increase in claim limit, you will also be covered for a wider range of healthcare conditions, more ward classes, pre- and post-hospitalisation expenses, and medical coverage outside of Singapore.

MediShield Life, for instance, is a mandatory health insurance offered by Singapore's Ministry of Health (MOH), with coverage for all Singaporeans and Permanent Residents (PRs) – but it has its limitations such as a S$100,000 claim limit per year, access to only class B2 and C wards in public hospitals, no coverage for maternity-related conditions, hospice, and moreAn Integrated Shield Plan (IP plan) basically serves to increase your annual claim limit for your MediShield Life plan – therefore increasing your healthcare coverage. MediShield Life's annual claim limit is only S$100,000 but an Integrated Shield Plan's annual claim limit may run up to S$1,000,000 instead. With the increase in claim limit, you will also be covered for a wider range of healthcare conditions, more ward classes, pre- and post-hospitalisation expenses, and medical coverage outside of Singapore.

Company Insurance

![]() Your employer’s policy may also have a variety of limitations such as deductibles, sub-limits, or co-insurance, and the probability of you leaving the job or facing retrenchment. Having your personal health insurance or Integrated Shield Plan (IP) will give you a plan to fall back on.An Integrated Shield Plan (IP plan) basically serves to increase your annual claim limit for your MediShield Life plan – therefore increasing your healthcare coverage. MediShield Life's annual claim limit is only S$100,000 but an Integrated Shield Plan's annual claim limit may run up to S$1,000,000 instead. With the increase in claim limit, you will also be covered for a wider range of healthcare conditions, more ward classes, pre- and post-hospitalisation expenses, and medical coverage outside of Singapore.

Your employer’s policy may also have a variety of limitations such as deductibles, sub-limits, or co-insurance, and the probability of you leaving the job or facing retrenchment. Having your personal health insurance or Integrated Shield Plan (IP) will give you a plan to fall back on.An Integrated Shield Plan (IP plan) basically serves to increase your annual claim limit for your MediShield Life plan – therefore increasing your healthcare coverage. MediShield Life's annual claim limit is only S$100,000 but an Integrated Shield Plan's annual claim limit may run up to S$1,000,000 instead. With the increase in claim limit, you will also be covered for a wider range of healthcare conditions, more ward classes, pre- and post-hospitalisation expenses, and medical coverage outside of Singapore.

Integrated Shield Plans: Which Treatments and Illnesses Are Covered?

Integrated Shield plans usually covers diagnosis, pre- and post-hospitalisation, critical illnesses (the number of critical illnesses covered vary from insurer to insurer), pregnancy complications, newborn congenital abnormalities, organ transplant, psychiatric treatments, surgeries that cost more than the MediShield Life cap of $2,600, hospital stays at A wards or even private hospitals.

Hospitalisation Ward

If you’re hospitalised, you’ll be staying in either a private or public hospital ward – which, like hotels, charges you for every night you stay, the services you use, and a bunch of miscellaneous fees. If you’re in the Intensive Care Unit (ICU) wards? It’s so much more expensive right? Most Integrated Shield Plans (IP plans) will cover ICU stays too.

Community Hospitals

Before you are discharged from the hospital, if your attending doctor at the hospital refers you to be transferred to a community hospital for further medical treatments and care, your community hospital stay can be filed for claims with your Integrated Shield Plan.

Inpatient Psychiatric Treatments

If you were hospitalised and you receive psychiatric treatments during your hospitalisation stay, the expenses incurred from these inpatient psychiatric treatments can be filed for claims – usually subject to a fixed coverage limit.

Surgeries

If your doctor tells you that you will need to be hospitalised to go under the knife for a surgery, ask your doctor if the surgery is in the Ministry of Health’s Table of Surgical Procedures 1A to 7C. If it is, then rest assure your surgery, surgical implants, including Gamma Knife radio surgery, will be eligible for claims under your Integrated Shield Plan. If you have a day surgery, however, you will need to check if your health insurance plan covers day surgeries – and any terms and conditions that may limit your day surgery coverage limit.

Outpatient (Not Hospitalised)

So, generally you need to first be hospitalised to be even eligible for any claims from your Integrated Shield Plan (IP plan). However, the IP plan also covers outpatient long-term illnesses’ treatments that you don’t usually get hospitalised for – such as kidney dialysis erythropoietin, cancer radiotherapy, chemotherapy, immunotherapy, and stereotactic radiotherapy. Other claimable outpatient treatments include immunosuppressants for organ transplant patients, and long-term parenteral nutrition (what you may know as tube feeding).

Pre-Hospitalisation Treatments

You must have heard of this term: pre- and post-hospitalisation. If your hospitalisation stay and the treatments you received during your stay have all been approved by your insurance company for claims, then you can start filing your pre-hospitalisation treatments for claims. That means, if you have been visiting the doctor for the same illness even before you were hospitalised, you can submit the receipts for claims within 180 days (or lesser, depends on your plan).

Post-Hospitalisation Treatments

When you’re about to be discharged from the hospital, chances are your doctor will ask you to schedule another appointment for follow-up treatments. While you may most likely come back to the same hospital, some doctors may refer you to other medical centres, clinics, or even Traditional Chinese Medicine (TCM) clinics for post-hospitalisation treatments. If your plan allows, and your doctor referred you to an insurance-approved clinic, you will be able to claim these treatments’ bills.

Major Organ Transplants

If you are receiving or donating one of your major organs in a hospital that’s recognised by your insurance company, you will be able to claim part or the full sum of your transplant medical expenses – depends on the coverage limit for organ transplants that's stated in your policy contract.

Pregnancy Complications

If you are a female with an IP plan, some insurance companies do allow you to make claims if you were to run into pregnancy or delivery complications – not all, just some complications. The type of pregnancy complications you can claim for differs from insurance company to company – some may offer none, some may offer 6 conditions, while some offer up to 36 pregnancy-related complications.

Congenital Abnormalities

If you were to be diagnosed with and treated for congenital abnormalities, you may be able claim these medical treatment expenses up to the coverage limit listed in your policy.

Why get an IP Rider Plan?

Regardless of whether you have MediShield Life or Integrated Shield plan — once you’re hospitalised, you’ll need to pay a certain portion of your hospital bill out of pocket or Medisave. The purpose of IP riders is clearly to reduce the deductible and the co-insurance or co-payment portion of your hospital bill so as to keep it as low as possible. This portion is made up of the following below. On the other hand, there are also riders that provide extra benefits like hospital cash benefits, medical coverage and even ambulance rides.

Deductible

![]() This is like the excess in car insurance — you need to pay this the first time you get hospitalised in a policy year before the insurer will pay the rest. It’s either $2,000 (B2 ward), $2,500 (B1 ward) or $3,500 (A ward/private).

This is like the excess in car insurance — you need to pay this the first time you get hospitalised in a policy year before the insurer will pay the rest. It’s either $2,000 (B2 ward), $2,500 (B1 ward) or $3,500 (A ward/private).

Co-insurance

![]() You also have to co-pay 10% of the hospital bill regardless of the deductible.

You also have to co-pay 10% of the hospital bill regardless of the deductible.

IP Riders offset these costs

![]() All IPs offer “riders” (add-ons) that reduce those costs down to just 5% co-insurance. IP riders are add-ons to your Integrated Shield Plan that give you more coverage/benefits.

All IPs offer “riders” (add-ons) that reduce those costs down to just 5% co-insurance. IP riders are add-ons to your Integrated Shield Plan that give you more coverage/benefits.

Get your personalised Insurance Plan here

Health Insurance Comparison

MediShield Life is kind of like the most fundamental layer of health insurance in Singapore, so other plans like the Integrated Shield plan (IP), IP riders, international health insurance plans (local or global providers) can complement your most basic healthcare coverage. If you’re still unsure about these plans and trying to differentiate them, here’s a quick comparison between the different types of health insurance plans available in Singapore.

| Type of health insurance plan | What it is | Payment mode |

|---|---|---|

| MediShield Life |

| MediSave |

| Integrated Shield plan (IP) | IPs covers you at A wards or even private hospitals but it comes at a higher premium which can be deducted from your CPF MediShield (up to the MediShield withdrawal limits). | MediSave |

| IP Riders | IP riders are optional, so you can “add on” these riders to your place to get wider coverage, and minimise any extra healthcare costs or enhance certain types of coverage you may need. | GIRO, cheque or cash |

| International health insurance plan (local and global providers) | You’re paying for a much wider healthcare coverage plan that usually includes inpatient and outpatient treatments, routine check-ups, chronic conditions, maternity coverage, newborn coverage, dental benefits, vision coverage, evacuation and repatriation coverage, and more. | GIRO, cheque, cash, credit or debit cards (Visa and MasterCard) |

How do I pay for Health Insurance?

This may be confusing for most. Here's a breakdown of how you can pay.

Methods to pay

Using MediSave to pay

When you pay the monthly premium for your Integrated Shield Plan (IP), you are collectively paying for the premiums of both MediShield Life and the additional IP coverage provided by your private insurer. The MediShield Life portion can be fully paid by MediSave. The private insurance component can also be paid via MediSave – although not the full sum due to additional withdrawal limits MediSave has set. For those aged 40 years and below, the limit is S$300 per year. For those aged 41 to 70 years old, the limit is S$600 per year. For those aged 71 and above, the limit is S$900. If the premiums for the coverage by a private insurer exceeds the above mentioned limit, any excess has to be paid by cash. Finally, premiums of any additional IP riders cannot be paid with MediSave.

What if my MediSave is insufficient?

MediSave can be used to not only pay for your MediShield Life but also of those of your immediate family members. In the event that you have insufficient balance in your MediSave account, you can use one of your family members’ MediSave account to pay for your MediShield and any additional IPs. However, if you have insufficient balance in your MediSave account and have limited family support, you will be provided with the option to pay the outstanding premiums for your MediShield Life via installments.

Other modes of payment

Besides MediSave or cash payment, there are other modes of payment which are accepted by health insurance companies. These include credit card, Visa or MasterCard debit cards, or GIRO. Depending on what type of health insurance plans you choose, you may have the option to choose your payment frequency – monthly, quarterly, half-yearly, or yearly, via your preferred mode of payment.

If you are looking to arrange for a recurring GIRO payment, some insurers do offer the convenience of providing the Interbank GIRO Application form on their websites for you to download, fill it up and submit it.

Get the right plan for you today!

How do I apply for a Health Insurance Plan?

Applying for a Health Insurance Plan through MoneySmart

Do A Quiz

If you find downloading insurance policy brochures and comparing them side by side a hassle, our intelligent system can do the comparison for you. Answer some questions online and we'll have you going.

Speak To Our Insurance Specialists

After you submit your quiz, our expert insurance specialist team members may drop you a call to clarify your needs and explain your options to you. Seize this chance to ask our friendly colleagues the burning questions you may have about health insurance!

Apply And Purchase Your Health Insurance

Once you have spoken to our insurance specialists, considered your options, and planned your finances, you are ready to apply for your health insurance plan online through our portal.

Compare Health Insurance Plans with us

Health Insurance Beginner Guides

Here are 3 beginner guides that you can read and bookmark for easy reference:

Health Insurance in Singapore — Everything You Need to Know to Survive

With So Many Integrated Shield Plans Available, How Do You Decide Which to Choose?

Your MediSave Account in Singapore — How to Make the Most of It

Best Mental Health Insurance Coverage in Singapore – Which Insurers Cover It?

Health Insurance Glossary Guide– Breaking Down Complicated Health Insurance Jargons

Best Health Insurance With Dental Coverage– How To Choose?

Frequently Asked Questions

How much is health insurance in Singapore?

- The average cost of an Integrated Shield Plan (IP) that covers up to B1 ward for a 35 year old individual that does not smoke is S$83. The above mentioned cost does not include premiums for MediShield Life.

How does health insurance work in Singapore?

- All Singaporeans and Permanent Residents (PRs) are entitled to basic governmental health insurance called MediShield Life. You can opt to increase your healthcare coverage by getting additional health private insurance plans such as Integrated Shield Plans.

Can expats buy MediShield Life or Integrated Shield plans in Singapore?

- While expats do not qualify for the governmental healthcare insurance plan, MediShield Life, they can purchase the Integrated Shield plans from local insurance providers.

How much does it cost to see a doctor in Singapore?

- Based on the sample costs provided in government website MoneySense, a 3-day stay in a Class A ward in a public hospital costs about S$900, while miscellaneous hospital bills (e.g. doctor’s fees) can amount to S$3,200.

Do you need health insurance in Singapore?

- Medishield Life is a mandatory governmental health insurance plan that all Singaporeans and Permanent Residents will be automatically enrolled in and need to maintain. You may enhance your Medishield Life healthcare coverage by purchasing an Integrated Shield Plan from private insurers in Singapore.

Can you opt out of MediShield Life?

- You cannot opt out of MediShield Life unlike the previous MediShield scheme. You can choose to pay for your MediShield Life premiums using Medisave or cash.

What is an Integrated Shield Plan?

- An Integrated Shield Plan (IP) is an optional health coverage provided by private insurance companies such as AIA, AXA, Great Eastern, FWD, Prudential, Income, Raffles Health Insurance, and more.

How do I know if I have an Integrated Shield Plan (IP)?

- Log in to your CPF account on www.cpf.gov.sg and click on ‘My Message’. You will be able to see if you have any Integrated Shield Plans (IPs), and which insurance provider you have been registered with.

Is it compulsory to have an Integrated Shield plan?

- No, it is not compulsory to get an Integrated Shield plan (IP). All Singaporeans and Permanent Residents (PRs) have basic coverage from MediShield Life. You can opt for an IP if you want to stay in a class A or B1 ward in public hospitals or private hospitals, and want to extend your healthcare coverage.

Can I use MediSave to pay for my health insurance?

- Yes, you can use MediSave to pay for MediShield Life and Integrated Shield plan (IP). However, premiums of IP riders have to be paid in cash.

Will the Integrated Shield Plan premiums increase with age?

- Yes, premiums increase with age. Also, due to rising healthcare costs, the premiums for the private insurance component of the Integrated Shield Plans (IP) have been increasing by an average of 7% per year.

Can I have multiple Shield Plans?

- No. You can only use MediSave to pay for one Integrated Shield Plan for yourself at any point in time. This is because the IPs provide generally similar coverage, and hospital or medical treatment bills can only be claimed from one plan.

Should expats get health insurance in Singapore?

- Yes, it will be helpful as expats can be covered against any risks and excessive health expenses. The group health insurance plans provided by most companies to cover their employees may not be extensive enough for you and your family as expats. Moreover, you will receive medical coverage 24/7 wherever you fly to, have access to a dedicated personal health insurance advisor via a 24-hour hotline that is available anytime you may need assistance.

Are local or global health insurance providers better than Integrated Shield plans?

- This depends on what you really need. Whether it’s an Integrated Shield plan or a plan by a local or global health insurance provider, the type of insurance policy is ideal for you will depend on your current health situation, the cost and quality of the local health care system and hospitals, if you are settled in your country of residence or move frequently, how often you travel, and many other factors.

What are IP riders?

- They are optional add-ons to your IP. IP riders help to reduce your out-of-pocket costs or enhance specific types of coverage, complementing your MediShield Life plan and Integrated Shield plan.