Quick Guide to Understanding Endowment Plans in Singapore

Disclaimer: This page is meant for educational purposes only and not meant to be taken as personalised or professional financial advice. Please consult with a trusted professional before committing to any insurance plan.

What is an Endowment Plan?

An endowment plan is akin to a savings and investment component integrated into a whole life insurance plan, providing potential for guaranteed and non-guaranteed returns (depending on the insurer’s performance). With an aim to build wealth over time without compromising on essential life coverage, it provides a lump sum payout upon policy maturity, pre-specified interval or policyholder’s death. Collectively, all these features justify its higher insurance premiums than those of pure protection-focused plans like term insurance.

How Does an Endowment Plan Work?

All endowment policies pay out a guaranteed sum assured, which is the minimum amount received at the end of the policy term, regardless of market conditions. However, depending on the type of endowment plan chosen, you may also receive a non-guaranteed bonus on top of the sum assured—these come in the forms of participating and non-participating plans.

Non-participating endowment plans

Participating endowment plans

Common examples of non-guaranteed bonuses include: reversionary bonus, terminal bonus, cash dividends, and accumulation bonus.

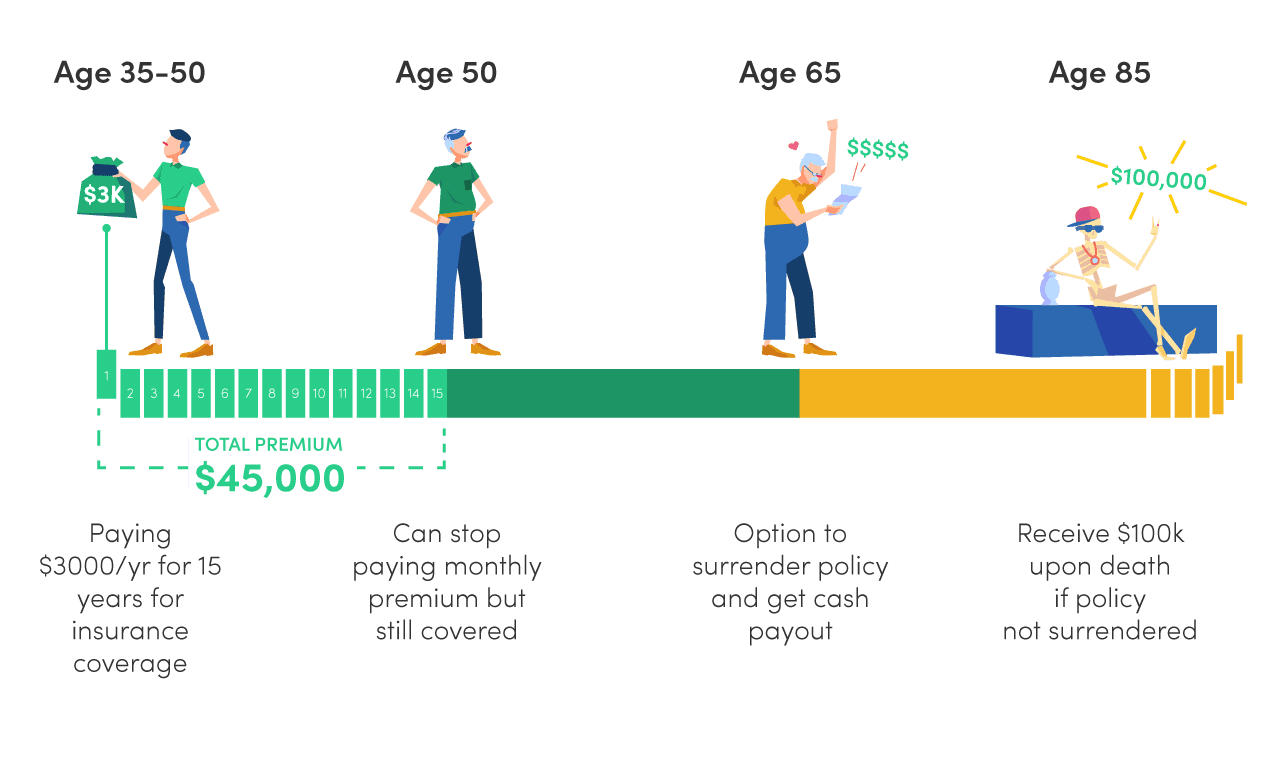

Remember: Endowment plans in Singapore are not whole life insurance policies. So when your premium payments end after 15 years, the policy continues to accumulate value until maturity. If the policy is surrendered at age 65, you’ll receive a cash value lump sum payment comprising:

Components of Endowment Plans

| Component | Participating | Non-participating |

|---|---|---|

| Coverage | All cover death Most cover total permanent disability Some cover major illnesses |

All cover death Most cover total permanent disability Some cover major illnesses |

| Policy term | Usually matures after a fixed period e.g. 10, 15, 20 years | |

| Cash value |

Comprises guaranteed sum + non-guaranteed bonuses Once declared, bonuses are guaranteed and payout depends on the performance of the participating fund If surrendered early, will only receive the guaranteed sum (cash value) plus vested (already declared) bonuses, which may be less than the total death benefit |

Comprises guaranteed sum only |

| Investment risk | Some risk If participating fund fails to generate returns, bonuses/dividends will be reduced |

Low risk |

| Premiums | Relatively higher premiums than term products; premiums are generally fixed throughout tenure and will not increase over time | |

| Riders | Possibility of adding riders to enhance policy benefits | |

Coverage

Sum assured

Similarly, a terminal illness claim would trigger the same payout, albeit treated as an “early death benefit”, prematurely terminating the policy once paid.

Cash value

Guaranteed cash benefits

Not to be confused with the sum assured, the guaranteed cash value consists of both guaranteed benefits and declared non-guaranteed bonuses (AKA reversionary bonuses).The guaranteed cash value increases gradually, before accelerating closer to maturity—reaching its guaranteed maturity value by the end of the policy term.

Non-guaranteed bonuses

Meanwhile, non-guaranteed bonuses refer to potential returns on investments distributed from the insurer’s participating fund, depending on its performance. These bonuses are not guaranteed until declared, and even then, how and when they are paid out depends on the type of bonus.Common types of bonuses include:

6 Things To Consider Before Buying An Endowment Plan

100% capital guaranteed

Total distribution cost (TBC)

Limited pay period

Depending on the policy terms and conditions, you may also be entitled to accumulated cash value in the event you surrender the policy at a specified age.

Surrender value

In general, this surrender value is less than the total premiums paid, especially in the early years.

Accumulated bonuses

On the other hand, terminal bonuses are non-guaranteed, one-time payouts added only at the point of policy maturity, surrender, or claim. Their amounts are reflected by the participating fund’s performance and remain unconfirmed until payout.

Maximise payouts

Reinvesting these payouts is ideal if you’re aiming to enhance your policy’s maturity value. Otherwise, withdrawing payouts early means receiving a lower overall payout when the policy matures.

Don’t Leave Life up to Chance!

Which Endowment Plan Should You Choose?

With so many insurance companies promoting their own range of whole life insurance plans with endowment policies, you may get a little overwhelmed with the plethora of choices. Fret not, we’ve the legwork for you and here’s a round-up of our 5 recommended endowment plans in Singapore.

Pros & Cons of Endowment Plans

Pros ✅

- Longer coverage than basic term plans

- Provides basic life coverage including death, TPD, and terminal illness benefits

- Dependents can benefit by enjoying lower premiums when getting insured from a younger age

- Accumulates cash value over the years comprising guaranteed benefit and non-guaranteed bonuses

- Offers participating and non-participating plan options

- Customisable for long-term financial goals like child’s education, retirement income, or other milestone savings

- Some plans allow reinvesting cash payouts to compound returns

Cons ❌

- Higher premiums than term plans

- Limited liquidity and often lower payout if policy is surrendered early

- Lower yields compared to ILPs

- Projected returns from non-guaranteed bonuses aren’t assured; can be reduced depending on participating fund’s performance

- TDC and other admin fees are bundled into the plan

- More costly than a basic savings plan and provides minimal scope of life protection anyway

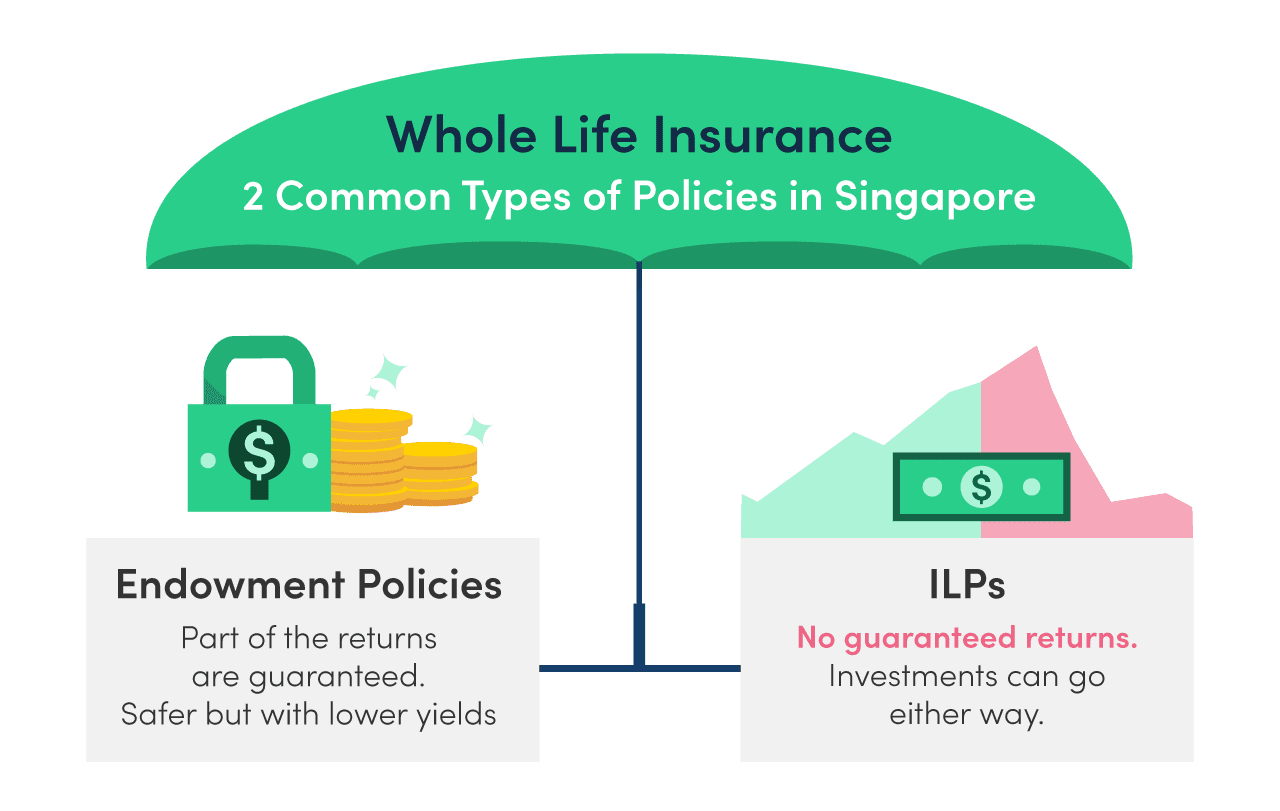

Endowment Plans vs ILPs (Investment-Linked Plans)

Unlike endowment policies, ILPs usually do not come with guaranteed values. While endowment plans offer a mix of savings, life protection, and potential investment bonuses (if participating plan), ILPs replace the savings with an investment component instead. A portion of premiums is used to purchase units in investment funds, where returns are then dependent on the fund’s performance.

As a result, there’s a higher risk involved as compared to endowment plans. Notwithstanding that, some still prefer ILPs because of the opportunity to invest and have financial protection through a single product. Plus, there’s a range of funds to choose from that caters to different investment objectives and risk appetite.

Ultimately, whether you choose an endowment plan or ILP, being clear on your financial objectives and your ability to afford their long-term costs is crucial. To learn more about the differences between the endowment plans and ILPs, check out this life insurance article.

Frequently Asked Questions

What is 100% capital guaranteed?

- It is a feature of an endowment plan that provides you 100% of your capital back when your policy matures. For such plans, the payout amount will at least be equal to the total premiums paid—provided you held the policy till its full term.

Are short term endowment plans better than long term ones?

- Yes and no. It really depends on what your financial goals are. Let’s say you’re just looking for alternatives to savings accounts, fixed deposits and even Singapore Savings Bonds (SSBs), short term endowment plans may give you more returns than bank accounts, plus some insurance coverage.

Conversely, for other objectives like saving for your child’s education or retirement planning, a long-term endowment plan may be more apt, but it requires a longer period of commitment and consistent premium payments throughout the policy tenure. What are guaranteed cash values and non-guaranteed bonuses?

- Guaranteed cash values will be the guaranteed amounts of your policy or policies, which excludes the non-guaranteed bonuses you've accumulated during the duration of the policy.

Non-guaranteed bonuses only become guaranteed once declared. This is usually done annually and accumulates on top of your policy's guaranteed cash value over time. What's the difference between participating and non-participating endowment plans?

- Participating plan: Offers both guaranteed cash values and non-guaranteed bonuses (often paid as dividends) based on the performance of the participating fund.

Non-participating plan: Only offers guaranteed returns, with no additional bonuses. The payout is fixed and with no investment influence. How do I know if my endowment plan has a limited pay period?

- You may check with your insurer or read the terms and conditions of your endowment policy. It should state that your endowment plan with a limited pay period means you’ll only have to pay premiums for a limited number of years in exchange for a lifetime’s coverage.

What will happen if I surrender my endowment policy earlier than the end term?

- If you surrender your endowment policy early, you’ll receive the "surrender value"—the amount payable upon early termination. This amount is usually less than the total premiums paid, especially in the early years.

For participating policies, the surrender value typically consists of two parts: a guaranteed portion and a non-guaranteed portion (such as declared bonuses, if any), depending on the participating fund's performance. Are there waivers for endowment plan premiums?

- Yes, many endowment plans offer optional riders that waive future premiums if you're diagnosed with a critical illness, total permanent disability, or similar conditions.

Can I withdraw money from my endowment plan before it matures?

- Some endowments allow partial withdrawals, but doing so will reduce the policy’s cash value upon maturity or result in penalties.

Early policy surrender can also lead to losses, particularly in the initial years of premium payments. How long do endowment plans last?

- It varies across endowment plans. Short-term plans can range between 2 to 6 years whereas long-term ones can range from 10 to 25 years or more.

It depends on personal preference and financial goals. Are there any tax benefits associated with endowment plans?

- No, endowment plans do not qualify for life insurance tax relief.

Can I use my Supplementary Retirement Scheme (SRS) funds to purchase an endowment plan?

- Yes, you can purchase an endowment plan using your SRS funds.

However, do note:- Premiums paid through SRS funds are ineligible for additional tax relief since SRS contributions already receive tax benefits.

- 50% of endowment plan withdrawals from the SRS account are subject to tax, if withdrawn on or after the statutory retirement age prevailing at time of first SRS contribution.

What happens if I miss a premium payment?

- Missed premium payments can cause your endowment policy to lapse or reduce in benefits. Although some may have grace periods or offer automatic premium loans to keep the policy in force, it’s imperative to understand your policy’s T&Cs and be responsible with timely payments!