Why Trust MoneySmart?

Why Trust MoneySmart?

Key takeaways

COE prices have risen drastically since its inception in 1990.

There are 5 COE categories: A, B, C, D, and E.

Besides the overt premium prices, COE categories also differ in buyer profiles, bidding behaviours, supply and demand factors, quota allocations, and vehicle resale values.

COE price trends are highly volatile and are affected by LTA policies, prevailing market conditions, supply and demand, and other factors.

You can use a personal loan to finance a car purchase and COE, but there are certain trade-offs to consider.

As part of Singapore’s traffic management framework, the Certificate of Entitlement (COE) is another measure to manage road congestion and regulate the country’s vehicle population. There are 5 COE categories, from Categories A to E, each corresponding to different vehicle types and ownerships.

To learn more about COE categories and discover how vehicles are classified under them, keep on reading.

Understanding COE Categories: What They Are and How They Differ

Singapore's COE system divides vehicles into five distinct categories based on engine size, power output, and vehicle type. Understanding these categories and how they differ is essential before you bid.

Breakdown of the 5 COE Categories in Singapore

COE category | Vehicle classification | Vehicle type (with e.g.) |

|---|---|---|

A | Non-fully electric cars with engines up to 1,600cc + Max Power Output up to 97kW (130bhp) Fully electric cars with Max Power Output up to 110kW (147bhp) | Mid-range cars (e.g. Mazda 3 Sedan, MG4 EV, 7-seater Toyota Sienta Hybrid) |

B | Non-fully electric cars with engines > 1,600cc or Max Power Output > 97kW (130bhp) Fully electric cars with Max Power Output > 110kW (147bhp) | Larger or performance cars (e.g. BMW 3 Series, Audi A4, MG Cyberster EV, 7-seater Hyundai Palisade) |

C | Goods vehicle and bus | For business and commercial vehicles |

D | Motorcycles | Two-wheeled vehicles |

E | Open – all except motorcycles | Highest price, most flexible |

Among the 5 COE categories, Categories A and B are the most commonly bid for. Category A covers more affordable, mid-range cars, while Category B COE caters more towards larger or higher-performance vehicles with more powerful engines. As a result, it stands to reason that Category B COEs tend to command higher Quota Premiums, while Category A COE sees higher bidding activity.

On the other hand, Categories C to E are more niche. Categories C and D are meant for business/commercial vehicles and motorcycles respectively whereas Category E is the open category, a free-for-all if you will (excluding motorcycles).

Why not bid for Category E COE?

Category E COEs are typically more expensive than Categories A and B because they’re open to all vehicle types except motorcycles. Strong demand from dealers and businesses drives up prices and competition, making them less cost-effective for individual bidders.

In the April 2025 bidding round, Category E closed at $118,001, compared with $99,500 for A and $117,003 for B. The few-thousand-dollar difference might seem small, but the added competition and higher premiums often outweigh the benefit for individual buyers.

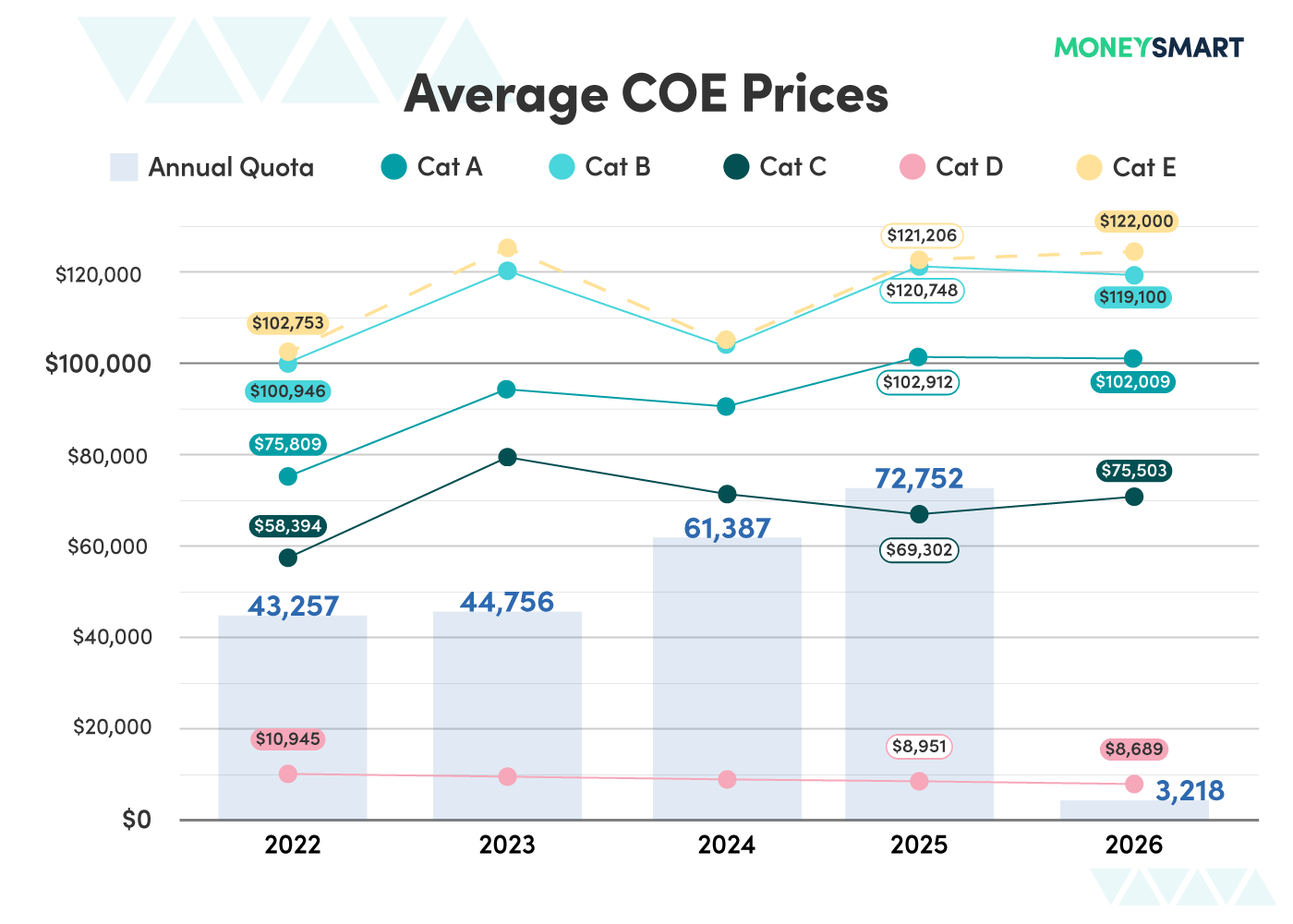

COE price premium history per category

Updated as of January 2026 Source: coe.sgcharts.com

What does engine size and horsepower mean for the COE category?

A car’s engine size and horsepower (or power output) directly impact its COE category classification. For context, engine size refers to the engine’s displacement (measured in cubic centimetres “cc”) and power output refers to the engine’s performance (measured in kW “kilowatts” or bhp “brake horsepower”).

To qualify for Category A COE, your car must minimally meet these requirements:

Petrol or diesel cars: Up to 1,600cc engines (1.6-litres) + up to 97kW (130bhp) maximum power output

Electric cars: Up to 110kW (147bhp) maximum power output

Cars exceeding these thresholds will fall under Category B, which typically involve higher bidding prices.

Key Differences between COE car categories

Beyond engine capacity, horsepower, and vehicle type, what other distinctions are there across COE categories? Well, here are a few more differences to consider when bidding on a COE:

#1: Quota allocation

Each COE grants the right to register, own, and operate one vehicle in Singapore. However, the number of COEs available in each category—the vehicle quota—varies during each open bidding exercise. These quotas are determined by the Land Transport Authority (LTA) and are influenced by factors like number of vehicle deregistrations and long-term transport planning.

Category A covers affordable, mid-range cars and typically gets a larger quota share because demand from everyday drivers is higher.

Category C is for commercial vehicles and usually gets a smaller, changing quota since fewer business vehicles are deregistered compared to private cars.

Category E is the open category for all vehicle types (except motorcycles) and sees the most fluctuation. Its quota varies widely due to intense competition from businesses, dealers, and private bidders.

#2: Bidding behaviour & buyer profiles

While we agree that COE bidding is competitive no matter which category, there are some categories that are more competitive and volatile than others. The nature of bidding activity is closely tied to the types of buyers they attract.

COE category | Customer type | Reason for demand |

|---|---|---|

A | Individuals and families | More affordable, fuel efficient cars (largely available to the mass market) |

B | Relatively more affluent individuals | Luxury, large-capacity and high-performance vehicles |

C | Companies, business owners, and dealers | Commercial vehicles like vans and lorries |

D | Motorcyclists | Motorcycles, including delivery/courier use |

E | Dealers, companies, fleet owners, parallel importers, individuals | Flexibility to apply any vehicle type (except motorcycles) |

MoneySmart Tip |

Fleet owners refer to individuals or businesses owning multiple vehicles for operational use, such as rental car companies, delivery services, or logistics providers. Parallel importers are third-party dealers who import foreign cars not officially sold by authorised distributors in Singapore. |

Category E experiences a highly competitive bidding environment across multiple market segments, making it challenging to out-bid and secure a COE here.

#3: Resale value impact

A vehicle’s COE category can significantly influence its resale value in Singapore. Generally, the hierarchy of vehicle resale value is as follows (from strongest to weakest): Category B > A > E > C > D.

Resale ranking | Why? |

|---|---|

1 (Best value) Category B | Strong prestige and desirability, even as secondhand cars Smaller but wealthier group of buyers with strong demand |

2 Category A | More affordable; appeals to the wider base of practical buyers |

3 Category E | Highly variable in resale value Heavily depends on type of vehicle registered |

4 Category C | Value depreciates due to heavier usage, wear-and-tear, and other business-related factors |

5 (Least value) Category D | Smallest market size and fastest depreciation |

MoneySmart Tip |

Category A and B cars retain better value during market downturns whereas Category E cars depreciate faster without sustained luxury or niche demand. |

#4: Transfer eligibility

Not all COEs are created equal when it comes to transferability. Whether a COE transfer can be executed has direct implications on a vehicle’s resale potential, flexibility, and market demand.

In Singapore, Category C and E COEs are transferable if bid under an individual’s name. However, if bidded under a company or organisation, it is non-transferrable

Meanwhile, Category A and B COEs are non-transferable for the first 3 months from registration. Additionally, vehicles being transferred should not have any outstanding financing or road taxes, regardless of category.

#5: Categorical pricing differences

COE prices are not uniform across all categories. Each category closes at different prices based on its own unique pricing dynamics influenced by the factors above.

In particular, Category B and E vehicles tend to see the most expensive COE prices. Category B tends to command higher Quota Premiums due to strong demand from affluent buyers for larger and higher-performance vehicles.

Similarly, Category E offers greater flexibility but experiences volatile prices, driven by prominent competition from dealers, parallel importers, and fleet buyers. While closing COE prices fluctuate month to month, this observation generally holds true.

What affects COE price trends and volatility?

While we know COE prices are highly volatile, now we can dive into more detail on what drives these changes exactly.

Supply and demand

For starters, supply and demand impacts prices greatly. Supply is determined by the vehicle quota released by LTA, while demand stems from buyer activity across individuals, businesses, and dealers.

Vehicle quotas are largely influenced by the number of vehicles deregistered, whether prematurely or upon COE expiry. When more vehicles deregister, the bigger the quota increases for the next open bidding exercise, potentially easing competition and lowering COE prices. Conversely, the fewer vehicles deregistered, the quota shrinks, tightening supply and pushing COE prices up.

Market conditions

Next on the chopping block is economic conditions. In times of prosperity and economic growth, more individuals and businesses are willing to bid more aggressively for cars. Hence, COE prices tend to spike during such periods of strong GDP growth or government incentives and rebates.

In contrast, during times of economic downturn, people have less disposable income and weaker consumer confidence, resulting in less demand for cars and causing prices to drop.

Government policies

Meanwhile, don’t underestimate the impact of LTA policy changes and price adjustments either. On occasion, LTA will revise how vehicle quotas are calculated or revise existing or release new policies with immediate effect on demand. Such policies include the Early Turnover Scheme or imposing tighter loan restrictions (more below).

As a result, such policy announcements will undoubtedly cause prices to spike or drop before or during the next bidding round.

MoneySmart Tip |

For experienced drivers, enjoy discounted Prevailing Quota Premium (PQP) for your COE when you opt for a cleaner, energy-efficient vehicle like electric cars over your existing car. |

Inflated competition from companies

It’s common for car dealers and fleet buyers, such as rental and leasing companies, to bulk-bid aggressively for stock vehicles, particularly during post-festive seasons. This concentrated demand artificially inflates competition and drives COE prices higher. As a result, individual buyers face greater difficulty securing COE bids during these peak periods of dealer activity.

Buyer behaviour

Beyond just numbers, buyer behaviour also plays a qualitative role. More often than not, car ownership in Singapore goes beyond functional needs. Despite Singapore’s robust and efficient public transport infrastructure, a significant segment of buyers still prefer purchasing cars to align with their lifestyle preferences and social aspirations. As such, this further sustains demand, inciting COE prices to continuously climb.

All these factors combined explain why Category E is more speculative and Category A caters more to the wider mass market.

Common mistakes to avoid when bidding for COE

While understanding the fundamentals is crucial before participating in your first COE bid, even seasoned drivers will admit—mistakes can happen, even if it isn’t your first rodeo. So take it from them; here are some common pitfalls to avoid when bidding for COE:

#1: Underestimating the final cost

Many first-time bidders forget that beyond just the Quota Premium (QP), there are additional administrative fees, taxes, and insurance costs involved in the bidding and ownership process. These include registration fees, Additional Registration Fee (ARF), excise duty, GST, car insurance, and COE registration charges.

Moreover, some overlook the possibility of urgently needing to renew their existing COE if their bid fails. In such cases, they’d be forced to pay a higher Prevailing Quota Premium (PQP) just to temporarily extend their old COE—often at a higher rate than current open market COE price.

These unexpected costs can easily catch bidders off guard and strain cash flow.

#2: Bidding too aggressively

Some buyers panic and overbid in a rush to secure a COE, but without careful budgeting, this can lead to unmanageable financial strain later on. It’s important to set a realistic reserve price and avoid caving to price fluctuations without proper research and a clear bidding strategy.

#3: Misunderstanding reserve price mechanics

Speaking of reserve prices, many bidders wrongly assume their bid must exactly match the latest COE price to succeed. In reality, bidding is more dynamic than that. While it’s recommended to bid above the expected QP to increase chances, blindly guessing or following past prices without understanding current market movements does not help your case. You’ll just be more prone to lose out on the bid or overpay.

MoneySmart Tip |

Always remember that the final QP is determined by the lowest successful bid within the available quota, not by matching a prevailing “target” figure. Set your reserve price strategically, factoring in market trends and demand patterns—not arbitrary numbers or emotions. |

Likewise, jumping into bidding without first monitoring a few months’ worth of Quota Premium trends can leave you blindsided as to whether the market is trending up, down, or stabilising. Knowing how price trends are fluctuating allows you to better strategise how to realistically bid, and whether it’d be wiser to wait for a better bidding window instead.

#4: Assuming Category E is “easier to win”

Some people believe that bidding under Category E automatically increases your success rate. But in reality, Category E can be even more volatile and expensive depending on dealer and business bidding behavior. That’s why in Singapore’s high-cost car market, it’s pertinent to do your due diligence before submitting a bid to avoid expensive regrets in the future.

Using a loan to fund your car and COE

While relatively uncommon, it is possible to use a personal loan to finance your car purchase and/or COE. After all, how the loan funds are used is ultimately up to the borrower’s discretion. Plus, in Singapore, there is a wide range of personal loans available to suit different financial needs—offering flexibility in interest rates, monthly repayment amounts, loan size, and loan tenures.

For instance, some traditional banks like Standard Chartered CashOne Loan offer highly competitive promotional rates starting from as low as 1.00% p.a., while other lenders such as Credible.sg Personal Loan may charge higher interest rates from 10.50%. Most loan tenures range up to 5 years, with some extending to 7 years.

So whether you need extra cash to cover your car’s upfront downpayment, monthly instalments, or securing a COE, a personal loan could be a viable solution.

Although, do note that under the Monetary Authority of Singapore (MAS) regulations, the maximum loan amount is determined by the car’s open market value (OMV):

For vehicles with an OMV less than $20,000: Up to 70% of OMV

For vehicles with an OMV above $20,000: Up to 60% of OMV

Personal loan | Interest rate | Total amount payable | Monthly repayment* |

|---|---|---|---|

Standard Chartered CashOne Loan | From 1.00% p.a. | $10,100 | $849 |

HSBC Personal Loan | From 1.83% p.a. | $10,220 | $852 |

Trust Instant Loan | From 1.00% p.a. | $10,100 | $852 |

POSB Personal Loan | From 1.99% p.a. | $10,268 | $856 |

DBS Personal Loan | From 1.48% p.a. | $10,268 | $856 |

GXS FlexiLoan | From 1.08% p.a. | $10,288 | $857 |

UOB Personal Loan | From 1.00% p.a. | $10,100 | $857 |

CIMB Personal Loan | From 1.00% p.a. | $10,100 | $867 |

Citi Quick Cash Program with Ready Credit | From 3.45% p.a. | $10,356 | $863 |

Credible.sg Personal Loan | From 10.50% | $11,050 | $950 |

*Assuming borrowing $10,000 over a 1-year tenure

Loan Repayment Calculator

See how much you need to pay back per month

You can expect to pay:

S$ 2,124.00 / month

*estimated monthly payment

There are also alternative loans called COE Renewal Loans. As its name suggests, these loans allow you to finance up to 100% of your COE’s PQP with flexible repayment tenures lasting between 7 to almost 10 years. Offered by both banks and licensed moneylenders, there is a decent variety of COE renewal loans available in Singapore.

Disclaimer: While banks can finance up to 60% or 70% of a car’s OMV, taking a personal loan contribute towards your Total Debt Servicing Ratio (TDSR)—and if it’s too high due to other outstanding debt—banks may be less willing to grant the maximum hire purchase loans. You end up having to fork a higher cash downpayment out instead.

Hence, always carefully assess your existing debt obligations (e.g. mortgage loans, renovation loans, credit card debt) before taking on more loans.

💡 MoneySmart Tip |

Use trusted online comparison tools like MoneySmart's personal loan comparison to review personalised rates, eligibility, and requirements across major banks in Singapore—helping you make a more informed choice quickly. |

(1).png)