Understanding The Dependants' Protection Scheme (DPS) In Singapore 2025

What Is A Dependants' Protection Scheme (DPS)?

Letter of notification

Welcome package

Health declaration form

How Does The Dependants' Protection Scheme (DPS) Work?

DPS policies can be a beneficial way to help you have a peace of mind with some level of financial protection at affordable premiums, since you can use your CPF Ordinary Account or Special Account savings to pay for the annual insurance premiums.

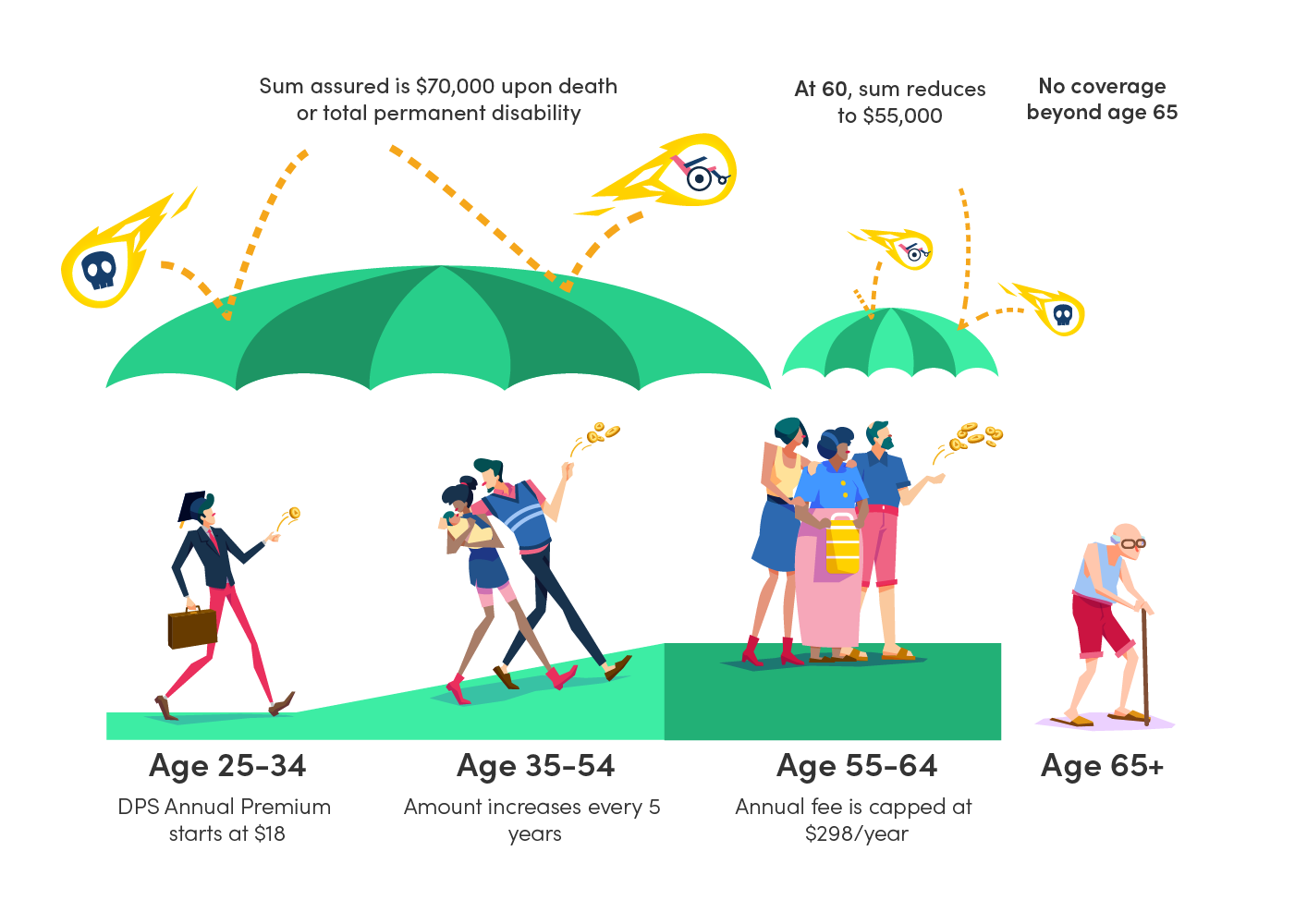

To get you started, let’s use an example to illustrate. Assuming that you’re 25 and you’ve just started on your first full time job. You’ll be paying $18 a year up to the age of 35, with premiums rising every 5 years up to $298 a year from the age of 55.

Coverage

The coverage that a DPS policy provides is pretty reasonable as it covers you for death, terminal illness and total and permanent disability (TPD) with a worldwide coverage period of up to the age of 65.

As the purpose of a DPS plan is to provide the basic coverage against the above three aspects, there is no cash value and there will be no payout at the end of the coverage period even if you’re still alive and well.

Payout assured (upon death)

The sum assured for you when you’re between 21 and below 60 years old is $70,000. The sum assured will be reduced to $55,000 when you turn 60 all the way till the day before you turn 65 years old.

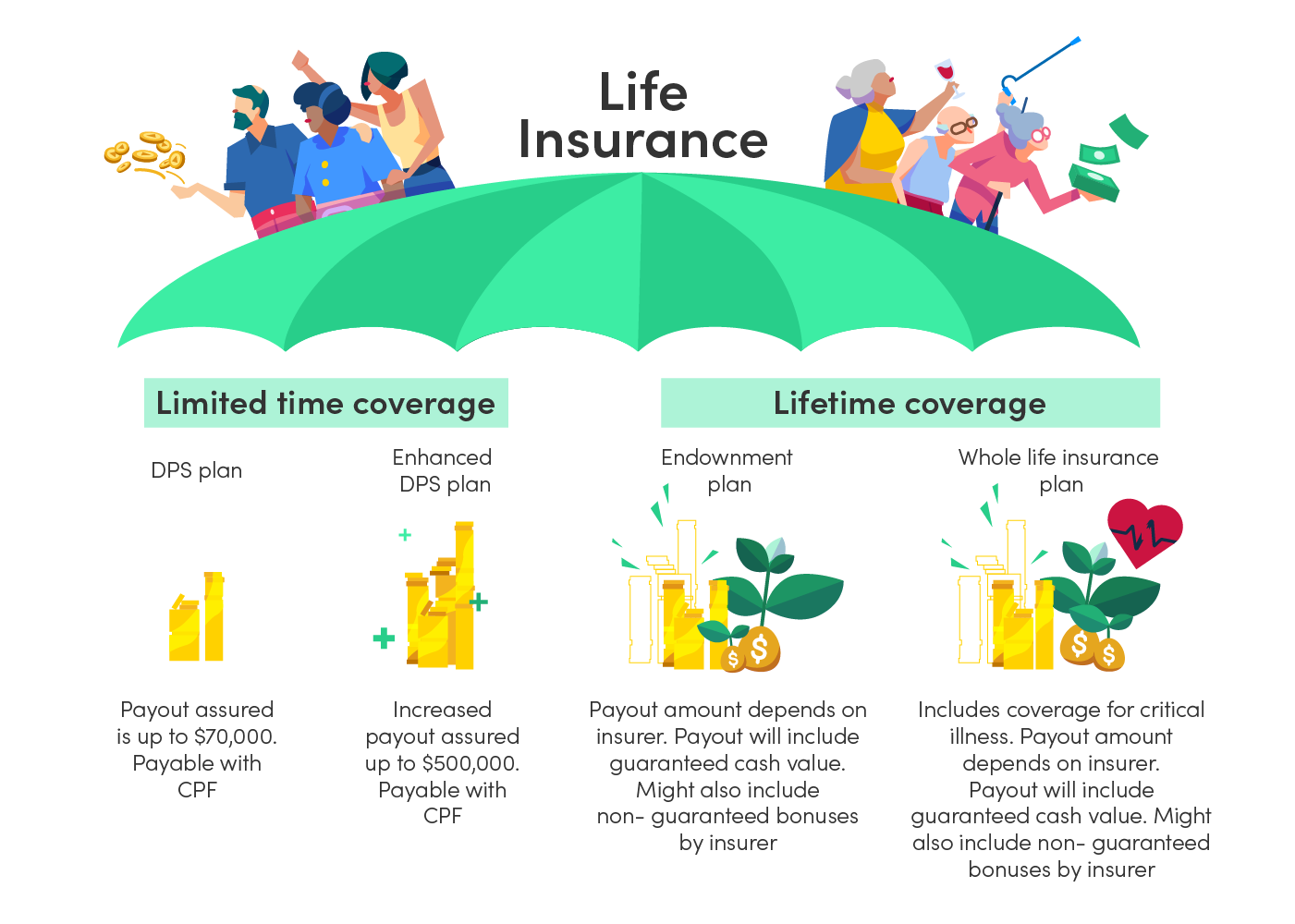

If you’re looking for some insurance plan with guaranteed cash value and non-guaranteed bonuses, the DPS does not offer these features, so you can consider other types of policies like endowment plans which enable you to withdraw a certain amount of money per year after your policy acquires cash value, or retirement savings plans that include a non-guaranteed bonus portion on top of the guaranteed cash payout amount.

Premium payments using CPF savings

You’ll have the option to pay in cash if you prefer not to have your DPS premiums automatically deducted annually from your CPF Savings. In the situation that your CPF Savings has insufficient funds to pay your annual premium, you can opt to lower your sum assured (the minimum sum assured is $5,000).

Exclusions

The general claim exclusions terms and conditions for the DPS include self-inflicted injury or suicide, criminal offences punishable by death, or a claim arising out of your own intentional criminal act. You will not be able to claim for any of these events if they occur within the first policy year of the cover.

Besides that, if you’re not in good health before the commencement of your DPS cover, or you’ve provided false or misleading information, you’ll not be entitled to any of the DPS benefits.

Looking for something else?

Pros And Cons Of The Dependants' Protection Scheme (DPS)

Pros

- More affordable premiums

- Flexibility to opt out of the DPS

- Choice of payments of premiums using CPF Savings or cash

- Lower premiums when getting insured from a younger age

- Enhanced DPS or term life insurance coverage options available if needed

Cons

- No cash value / accumulated cash payout over the years

- No non-guaranteed bonuses

- No investment opportunities

- Limited coverage, not a lifetime coverage

Dependants' Protection Scheme (DPS) vs Other Life Insurance

| DPS | Enhanced DPS plan | Endowment plan | Whole life insurance plan | |

|---|---|---|---|---|

| Coverage | DPSDeath, terminal illness, total permanent disability from 21 years old to 65 years old | Enhanced DPS planDeath, terminal illness, total permanent disability from 21 years old to 65 years old | Endowment planLifetime coverage for death, terminal illness, total permanent disability | Whole life insurance planLifetime coverage for death, terminal illness, total permanent disability and critical illness |

| Payout assured | DPSUp to $70,000 | Enhanced DPS planUp to $500,000 | Endowment planDepends on the insurer’s offer of the percentage of capital guaranteed, guaranteed and non-guaranteed bonuses | Whole life insurance planDepends on the insurer’s offer of the percentage of capital guaranteed, guaranteed and non-guaranteed bonuses |

| Guaranteed cash value | DPSNone | Enhanced DPS planNone | Endowment planYes | Whole life insurance planYes |

| Non-guaranteed bonuses | DPSNone | Enhanced DPS planNone | Endowment planYes | Whole life insurance planYes |

Buy The Best Term Insurance Plans Here

How Do I Claim From The Dependants' Protection Scheme (DPS)?

Inform Great Eastern Life of the incident/illness

Have the supporting documents ready for submission

The documents you’ll need to submit include:

- Original medical report, post mortem report and/or toxicology report

- Total and Permanent Disability claim form (available for download on Great Eastern Life’s website)

- Doctor’s statement document (available for download on Great Eastern Life’s website)

- Original receipt for the fee charged for completion of the doctor’s statement

- All available lab and test results

- Death claim form (available for download on Great Eastern Life’s website)

- Certified and original copy of the death certificate

- Letter from Immigration and Checkpoint Authority (ICA) for death occurring overseas Identity card and proof of relationship with deceased

- Doctor’s Statement if the death occurred overseas

- Last Will of deceased (if applicable)

- Original copy of policy report for accidental death

Approval of your claim and settlement

Frequently Asked Questions

Is the Dependants’ Protection Scheme compulsory?

- No. Although all Singaporeans and PRs are automatically entitled to the Dependants’ Protection Scheme (DPS), there’s a choice to opt out of it if you do not wish to be covered.

How much do I need to pay for my Dependants’ Protection Scheme (DPS) premium?

- It depends on your age. DPS premiums usually range from $18 to $298 per year. If you’re 21 years old, you’ll need to pay $18 a year up to the age of 35. By the time you’re 50, you’ll be paying $188 per year, with premiums rising every 5 years up to $298 a year from the age of 55.

Are there any claim exclusions for the Dependants' Protection Scheme (DPS)?

- Yes, the DPS claim exclusions include self-inflicted injury or suicide, criminal offences punishable by death, or a claim arising out of your own intentional criminal act. Any DPS member will not be able to claim for any of these events if they occur within the first policy year of the cover. Besides that, if you’re not in good health before the commencement of your DPS cover, or you’ve provided false or misleading information, you’ll not be entitled to any of the DPS benefits.

Is the DPS better than other term insurance plans?

Yes and no. It really depends on what your financial needs and goals are. Let’s say you’re just looking for a simple coverage for death, terminal illness and total and permanent disability (TPD), the DPS will suffice.

On the other hand, if you’re thinking of getting more comprehensive coverage, the enhanced DPS plan or other types of term insurance plans may be suitable to supplement your existing DPS.

Does DPS offer guaranteed cash values and non-guaranteed bonuses?

- No. Unlike endowment plans or whole life insurance plans which offer guaranteed cash values or non-guaranteed bonuses that increase your total sum assured, DPS do not offer any of these cash values or interest returns.

Do DPS premiums increase with age?

- Yes. For example, if you’re 21 and you’ve just started on your first full time job with CPF contribution, your premium will be $18 a year up to the age of 35, with premiums rising every 5 years up to $298 a year from the age of 55.

What will happen if I wish to cancel my DPS policy earlier than the end term?

- There is no cash value or interest returns payout when you cancel your DPS policy before the end term. You’ll need to download the Opt-Out Form and email the completed form to Great Eastern Life at dps-sg@greateasternlife.com to complete your cancellation.