Beginner Guide on Home Protection Scheme in Singapore

Homeowners who own HDB flats will probably be more familiar with the Home Protection Scheme, also known as the HPS, which is a mortgage term insurance for all CPF members. So as long as you've started working and have made sufficient CPF contributions, you’ll automatically be offered the option to be enrolled in the HPS when you buy your first HDB flat.

However, you have the choice to opt out of the HPS if you prefer to be covered by other types of private insurance plans including whole life insurance plan, term life insurance plan, or an endowment plan. A HPS policy is often more affordable than other types of private insurance plans, plus you’ll be able to use your CPF savings to pay for the annual premiums.

What Is The Home Protection Scheme (HPS) About?

Approved mortgage loan with HDB

Health declaration

HPS certificate

How Does The Home Protection Scheme (HPS) Work?

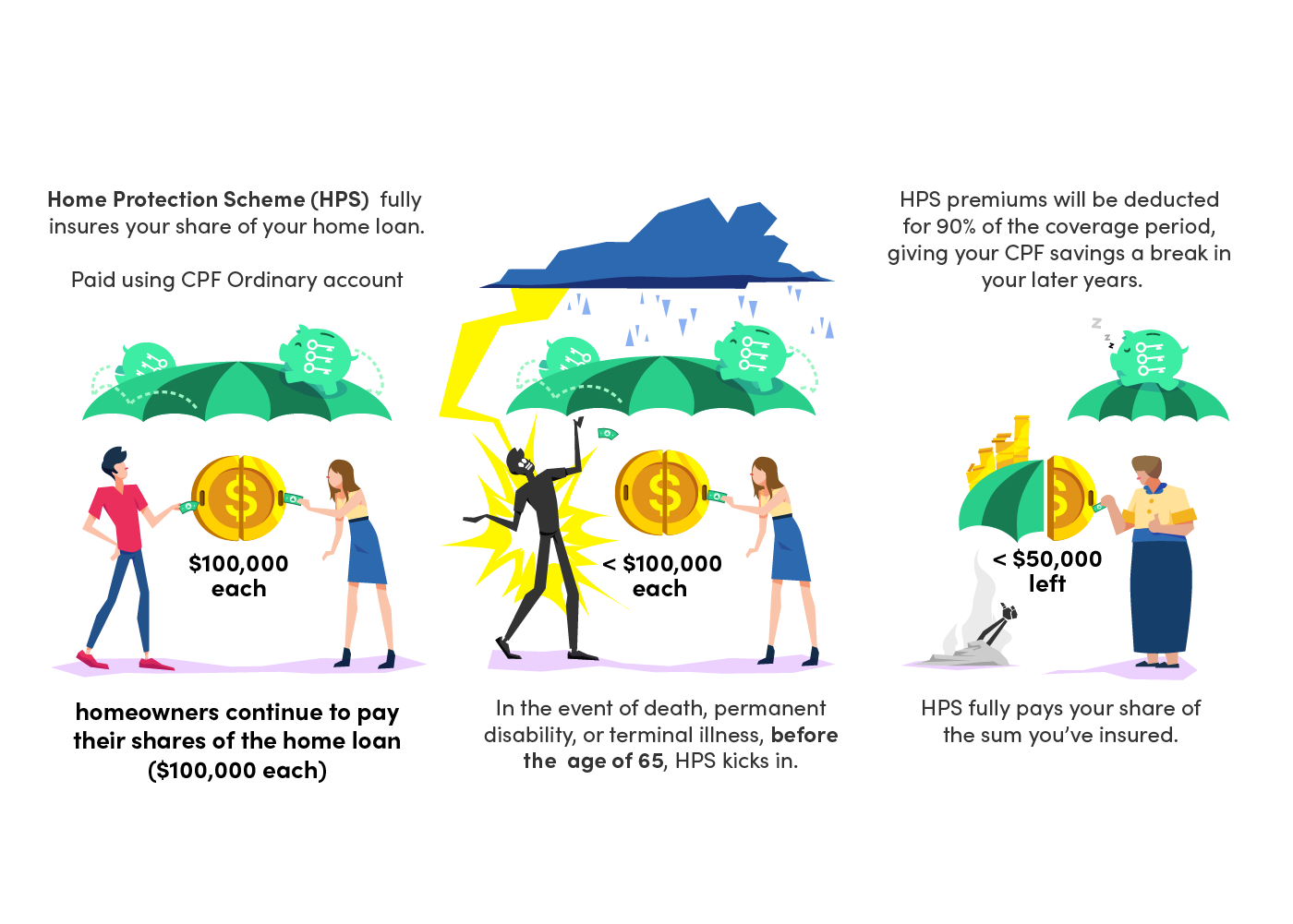

A great thing about a HPS policy is that it can help you be insured with a decent level of financial protection at affordable annual premiums which you can choose to use your CPF Ordinary Account savings to pay for. If you or one of your family members qualify for a claim, whether you or he/she gets diagnosed with a terminal illness, or becomes totally and permanently disabled, the HPS claim amount will be the remaining sum on your home loan.

For instance, you pass away while still owing $100,000 on your home loan. This $100,000 will be paid in full by the HPS that you’re enrolled in, at the same time your family do not have to worry about losing the flat or having to take over loan repayments after your death or illness.

Single or co-sharing homeowner

Total coverage of all the owners is at least 100% of the outstanding home loan by default. When you and your spouse pay equal amounts for your HDB flat, each of you will be covered for 50% of the loan. In the event of a claim, your HPS will give you the sum assured based on the share of cover that you and your spouse have applied for.

When there is insufficient balance in your CPF Ordinary Account to pay the premium required, you can tap on the CPF funds of your family member’s (only one that co-owns the flat with you i.e. your spouse/parent/child/sibling), but you’ll need to authorise CPF to use his/her CPF savings to pay for your HPS premium shortfall.

Coverage

Adjustment of HPS cover

There are several factors which may result in the need to adjust your HPS cover and these include:

- Capital repayment of your HDB loan or restructuring of the HDB loan

- Refinancing of your existing loan

- Sale of your HDB

- Full redemption of your HDB loan

- Changes in your share of loan repayment

These changes will lead to a new HPS cover issued to you, based on the new loan information/share of responsibility, and your premium will be adjusted accordingly to ensure that you're adequately covered. For any increase to your HPS cover, e.g. increase in cover period or sum assured, a health declaration and new application to increase your HPS cover will be needed to facilitate a reassessment of your eligibility for the HPS.

Premium payments using CPF savings

How Much Do Home Protection Scheme (HPS) Premiums Cost?

Your age and gender

Whether you’re tied to a HDB concessionary loan or bank loan

The outstanding housing loan on your flat

The loan repayment period of your flat

Home Protection Scheme (HPS) vs Other Mortgage Insurance

Being a new homeowner and having to learn about all the processes to get your HDB flat can get a little overwhelming at times. Moreover, with so many private insurance plans in the market besides the HPS, you’ll have to weigh the pros and cons of various options to help you arrive at the right decision.

It is great to start with the basics, which is the HPS, but you should also consider private mortgage insurance plans if you need something more to supplement your HPS. Here’s a quick overview of the pros and cons of choosing a HPS over most private mortgage insurance plans.

Pros

- More affordable premiums than those offered by private mortgage insurers

- Adjustable coverage

- Only 90% of the HPS cover period is payable

- Flexibility to opt out of the HPS

- Premiums can be paid using CPF Ordinary Account

- Alternative to tap on co-owner’s CPF funds if there’s insufficient balance in your CPF Ordinary Account for premium payments

- Lower premiums than most private mortgage insurance plans

Cons

- Not eligible for private property homeowners who have executive condominiums (ECs) or privatised HUDC flats

- Lower coverage as compared to private mortgage insurance plans

- HPS premiums are higher for those taking a bank loan instead of HDB concessionary loan

- Not transferable if you buy a new property

- No enhanced HPS plans available or riders for premium waivers and critical illnesses

How Do I Check My Home Protection Scheme (HPS) Cover?

There are a couple things to take note of if you need to check your HPS cover for reasons like capital repayment of your HDB loan, refinancing of your existing loan, sale of your HDB, changes in your share of loan repayment or others.

Here are 3 simple steps to check your HPS cover:

Get your Singpass details ready

You'll have to log into the CPF Home ownership dashboard with your Singpass details and click on "Protection against losing your home".

Check your coverage status

Apply for HPS if no status shown

If there isn't any "Protection against losing your home" in the dashboard, this means you are not insured under HPS at the moment. Thereafter, you may decide whether to apply for a HPS cover for your outstanding housing loan using your Singpass and you can do so online.

Frequently Asked Questions

Is the Home Protection Scheme compulsory?

- Yes and no. It is only compulsory for those who are using their CPF Savings to pay for their HDB flats’ monthly instalments.

How much do I need to pay for my Home Protection Scheme (HPS) premium?

It depends on a few factors such as your age, gender, whether you’re tied to a HDB concessionary loan or bank loan, the outstanding housing loan on your flat

Your age affects your HPS premiums as the more mature you are, the higher your premium. HPS premiums also tend to be higher for males than females, and higher for those taking a bank loan due to the long-term volatility of bank loans.

What are the claim exclusions for the Home Protection Scheme (HPS)?

- The HPS claim exclusions include:

- self-inflicted injury or suicide

- criminal offence punishable by death, or the claim arose out of member's own intentional criminal act

- not in good health before the commencement of HPS cover

- provision of false or misleading information

- claim arose from wars or any warlike operations or participation in any riot

Is the HPS better than private mortgage insurance?

Yes and no. It really depends on your mortgage needs and your financial capacity to pay back insurance premiums. HPS offer more affordable premiums than those offered by private mortgage insurers and you only have to pay 90% of the HPS cover period, plus your HPS premiums can be paid using your CPF Ordinary Account funds.

On the other hand, if you're thinking of getting more comprehensive coverage and don't mind paying higher premiums using cash payments, then private mortgage insurance plans may be more suitable for you.

Do HPS premiums increase with age?

Yes. Your premiums will get higher as you turn older each year. You may refer to CPF Board's HPS Premium Calculator here to estimate your annual premiums.

Can I cancel my HPS policy earlier than the end term?

This depends on the remaining for the co-owner(s) of your HDB flat. It must be at least 100% after the termination of your HPS policy, if not your request for the termination of your HPS policy will be rejected, You may apply to terminate your Home Protection Scheme (HPS) cover online via my cpf digital services.